Exchange Rate and International Relative Prices

Exchange Rate and International Relative Prices

We define exchange rates, understand their changes and get the basics right.

When we hope to travel outside our country, we often seek countries where it would be cheaper to travel, cheaper prices for staying in nicer hotels, cheaper flight tickets. Often, we keep track of prices so that we can get the best deals on all of these and pre-plan our holidays. But the most important determinant is the exchange rate between our currency and the currency of the country which we intend to go to – and certainly to have fun! It is also likely that we choose countries which have weaker currencies than ours so that we can afford the trip. This tells us that exchange rate matters for our short-term travels.

It matters even for our longer-term work or study decisions. My students often choose countries where the Indian rupee is not as worse-off as it is for others. This makes Australia and Canada a very attractive destination when compared to universities in Europe. This is not to say that exchange rate is the only reason for taking such decisions but can be relatively important if you are on the financial edge of your seats.

Similarly, when there are interactions which occur across countries mediated by producers, governments, politics and policies, all track exchange rate with significant interest. One could think of other interactions across countries which are realistic and have an exchange rate variable in the optimal decision.

While most spot decisions which involve international transactions are bound to feature exchange rates, even inter-temporal dynamic decisions are likely to be contingent on movement of exchange rates. For instance: if you want to invest your money in another country, most likely the ones that are growing now – China and India, you are also interested in their exchange rates. If you invest US dollars in China, and if the Chinese Yuan appreciates against the greenback, then your return needs to cover the loss of a Yuan appreciation. Hence the decision of where to invest is not a simple one, but one which requires you to make an assessment about how the exchange rates are going to hold up by the time you decide to get your money out of the country for its actual “use” - consumption.

Given this magnitude of importance of exchange rate for individual decisions – both static and dynamic, it is likely that these would add up to be quite important even at an aggregate level. Exchange rates can explain part of the variation in trade and commerce across countries, movement of people and movement of finance. How much of these events can it explain has been at the heart of such debate and is often contextual. I also think it is very country specific, yet one would like to theorize the general behavior of this variable to draw connections in theory. Before we think about the relevance of exchange rates for these decisions, its best to define exchange rates accurately.

Defining exchange rates

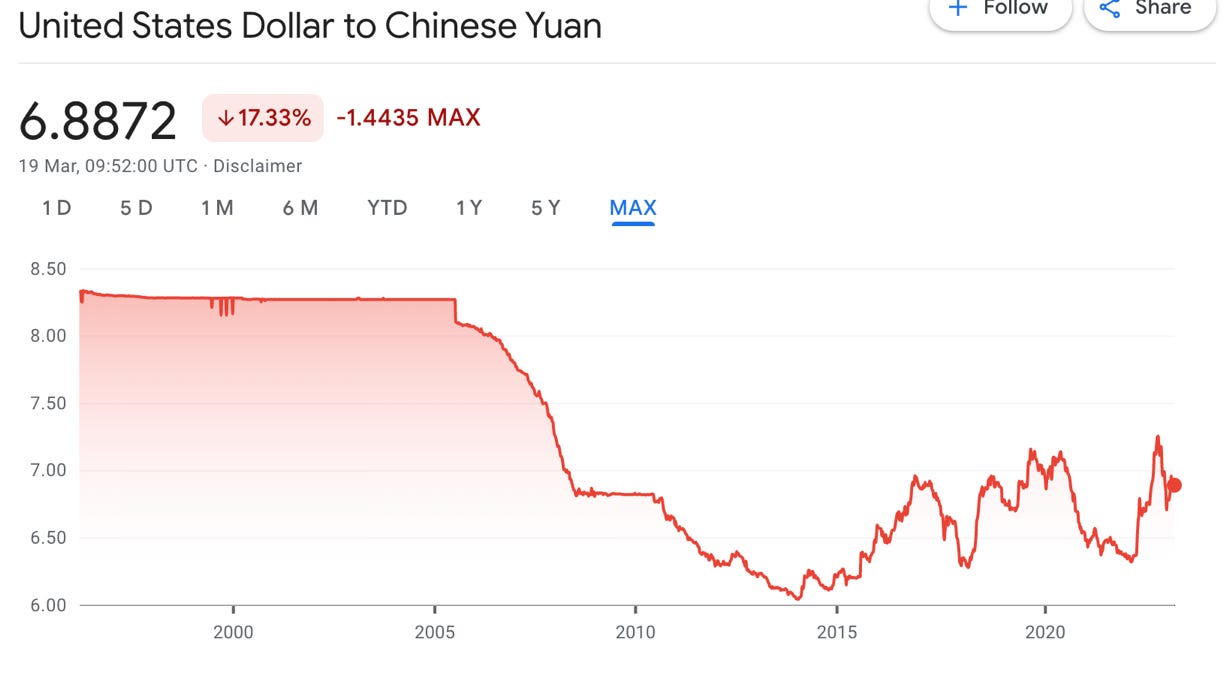

Consider the following exchange rate drawn from a simple google search:

This tells us how many Chinese Yuan can be bought with one United States Dollar. The x-axis is time which starts in late 1990s, and goes on till the date on which this screenshot was last taken – 19th March 2023. The y-axis tells us the conversion or exchange value. Its most recent value tells us that one could exchange one USD to 6.88 CNY. Before we get into the definition of exchange rates, we need to fix the point of view. Let us consider China to be the home country. If this is the case, it tells me how many units of the home currency (CNY) can be purchased by one unit of the foreign currency (USD). This is the American definition of exchange rate where the home country is China, denoted by E(Y/$) or E(1/2), where 1 represents the home country and 2 represents foreign country. The 1/2 reminds us that the unit of measure is 2’s currency i.e. one unit of 2’s currency gives me how many units of 1’s currency.

On the other hand, if we were to ask the opposite question: how many units of USD can I obtain with 1 CNY, then the answer would be written as E($/Y) or E(2/1) and is called the European definition. This measures identical information, but the base is now a unit of CNY. If I search for this information in google, I get the following:

Notice that the x-axis still measures the same duration i.e. slightly before 2000s and ends up at 19 March 2023. The y-axis is now scaled down to the unit of CNY. The value of 0.1452 tells us that one CNY gives you only 14 cents. Again, both these numbers give you identical information – they tell us how we could convert USD to CNY or vice-versa. If you had 100 USD, you would get 688 CNY. If you had 688 CNY, you would get 100 USD. This is represented as

Percentage change in exchange rates

Now that we have a working definition of exchange rates, we need to measure their changes appropriately. While all the optimal decisions which are static i.e., how much to buy from another country, when to convert my currency etc. can be undertaken by monitoring these exchange rates, it is not sufficient for dynamic decisions – what happens to exchange rates when I take my money out six months from now? In such a scenario, it is the gap between the current and the future exchange rate that matters for me. To be precise, it is the gap between the current exchange rate and the expected future rate which matters for my decisions now. My eventual gains are certainly dependent on how the exchange rate turns out when I think of withdrawals. This implies that we have three rates which helps us understand the current decision and the realized gain or loss. The first is the current spot rate i.e. E(t), the expected rate E(t)e – which is the expectation that you form about the spot rate in time t+1, and the actual spot rate at time t+1, E(t+1). The timing of these rates is crucial i.e. you cannot get to know the E(t+1) till you reach time period t+1.

This also gives us two percentage changes which measures expected change and the actual change – realized change because they only occur when the future is “realized” or lived. (a) This is a simple percentage change of exchange rate between two time periods, today and tomorrow. One can calculate compound growth rate, but this makes sense only if there is compounding of the underlying variables. (b) Today is denoted by t, and tomorrow is just t+1. One can think about any duration of change as a single unit of time can be weekly, fortnightly, monthly, quarterly, or annually. (c) Since we do not know the t+1 exchange rate, we must substitute it with what we expect or with the realized change, but only to calculate such a change at time t+1. At time t, I can only make an informed guess about t+1.

The expected percentage change of exchange rate measures a portion of exchange rate changes which were anticipated by the decision maker. In fact, everyone who decides to invest overseas has an expected exchange rate and could calculate the implied percentage change in the exchange rate. This is calculated by replacing with where the e denotes expected with the following formula:

Finally, when you reach , then you can retrospectively calculate a percentage change as follows:

This is the actual change which you could observe in the exchange rates. This realized percentage change is also fairly important because it tells you how you got your expectations wrong i.e., by calculating the error in actual and expected percentage changes one could get an assessment of one’s forecast error.

Trade Weighted Exchange Rates

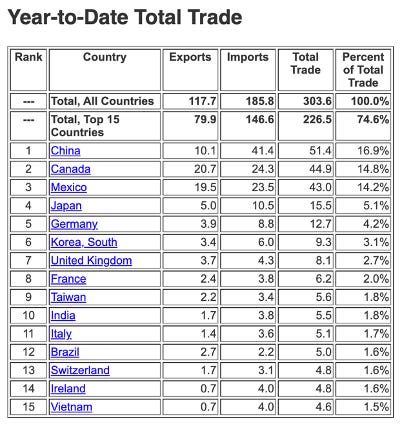

Now you know about defining exchange rate and measuring actual and expected changes to exchange rates. However, if you look at a country, you observe that it trades with not just one but many countries together. For instance, the trade with its top 15 partners for USA for Jan, 2017 (panel a) and October 2022 (panel b) tells us that they are significant. Even though you observe difference in the relative importance of countries in the two panels, the composition is relatively stable. Notice that we have only shown trade interactions, and it is likely that USA has finance interactions with these countries which dwarf these trade numbers.

This points to the idea that there is no single exchange rate which is important, but it is likely to be a combination of many important exchange rates which tells us about the interaction of a country with its trading partners. Secondly, the level of such exchange rates is unlikely to be important because it would be hard to interpret the average. Hence for a country we are likely to be interested in the movement of this average. If we want an average percentage change for the nominal exchange rate for many pairs of exchange rate, we calculate the nominal exchange rate as follows:

This gives us an average where is the nominal exchange rate between country 1 and country i at time t+1. There can be n such countries, usually a country trades with around 130 odd countries on an average, but the magnitude of trade becomes small or next to negligible after the top 30. The ratio then tells us the percentage change between the two exchange rates from time t to t+1, and the product of such ratios takes the geometric average instead of the simple arithmetic average. This, however, does not make complete sense.

When we calculate an average, we put the same weight on the Chinese Yuan as we do to the Vietnamese Dong, even though USA trades with China is a 15% while that of Vietnam is 1.5%. Putting equal weight on a Dong depreciation and a Yuan appreciation would not reflect how US trade gets affected by a Yuan appreciation rather than a Dong depreciation. To correct this, we weigh these changes with the trade shares of these country pairs to obtain a nominal effective exchange rate as follows:

An equivalent representation can be used for smaller changes in exchange rates using a weighted arithmetic mean as

This is the number which is of interest when we examine the exchange rate for a country i.e., the movement in its trade weighted nominal effective exchange rate.

Using exchange rate to understand goods and labor flows.

The NEER can now be thought as something like the nominal exchange rate aggregated at the country level. We need not examine the exchange rate between USD-CNY, or between USD-Euro separately, but instead observe changes in the NEER for USA to understand the position of USD to other currencies.

The data shown above raises important questions. Why does the NEER go up from 2012 to 2022? What does it mean for US trade with other countries? What does it mean for the movement of labor or finance? The broad upward trend for NEER tells us that the US dollar has been appreciating with respect to the currencies of its trading partners. This implies that if a US consumer want to import from the rest of the world, they would find it cheaper to do so, especially when compared to the 2008 USD levels. The exact opposite happens to consumer from other countries. They would find it more difficult to import commodities produced in USD or priced in USD because they experience a depreciation of their currency. The broad trend is one of average appreciation of USD. This fails to tell us about bilateral relation between US and a particular trading partner. For these purposes NEER is not as effective.

Appreciation, Depreciation and The Importance of Exchange Rates

Let us go back to the definition and the first figure which gives us the bilateral exchange rates between US and China. Let us zoom into the last five years – figure reproduced below. On 30th March 2018, one USD gave us 6.2856 CNY. Now that value has gone up to 6.8982. That is a 10% appreciation of the US dollar. What does this mean for the US consumer?

In general, the appreciation for the USD implies that its consumer finds the USD more powerful because they can buy more commodities with one USD than what they could do five years back. This creates a propensity for them to import greater goods from China. On the other hand, Chinese consumers are likely to find US goods more expensive and hence either reduce their demand for US goods or substitute these goods with goods produced elsewhere. How much would a 10% appreciation of the USD translate to changes in trade flows is an empirical question.

We can generalize this statement. An appreciation of a country’s currency makes its exports expensive and imports cheaper. Hence for an importing country – such as the US, an appreciation is likely to be beneficial. On the other hand, a depreciation of a country’s currency makes its imports more expensive and exports cheaper. Hence for an exporting country – such as China, a depreciation of its currency is likely to be beneficial. Further, since the appreciation of USD, more American travelers will find it cheaper to travel to China than before, hence lead to an additional tourist movement into China. On the contrary, the relative depreciation of Chinese Yuan prevents more Chinese travelers to visit USA. This is the point of observing bilateral exchange rates – it helps explain potential trends in goods, labor and finance movements which is stimulated by this additional appreciation in USD.

Finally, the USD comes with a caveat because unlike other currencies, USD is the reserve currency i.e., most international transactions occur in USD. For us, this implies that while general direction of appreciation and depreciation might indicate an increase or decrease in demand for a currency, this might not be applicable for the USD. Moreover, we examine exchange rate mostly in an environment of trade i.e., how it impacts imports or exports. However, the direction of USD might be affected not as much by the buying and selling of US consumers and producers but by other factors which create or suppress additional demand for USD.

Some exchange rate questions.

I close this post with some questions which I bother me and some facts which throw the standard exchange rate theories out of the window. While most of the actions around exchange rates occur in countries which allow these actions to occur, most of the exchange rates are fixed by governments. One caveat to this fact is that countries which have flexible exchange rate have lion’s share of the global trade – most developing countries do not allow exchange rate to be market determined. For instance, while China has recently (since 2015) reverted to a market determined exchange rate, Hong Kong still maintains a sharp control over its dollar. If most exchange rates are fixed by the government, on what basis do they fix these rates? And does this imply that relative prices in such an economy are no longer market determined? If so, how does it help in their policy?

Moreover, there are certain exchange rates which fail to make sense in terms of magnitude. First, Indonesia abandoned its fixed exchange rate after the Asian Financial Crisis in 1997. You can see its exchange rate shoot up. Now it stands at 1 USD = 15,392 Indonesian rupiah. We do not have a clear theory on how to interpret this absolute number as exchange rates, but it is safe to say that such a conversion is in the unreasonable realm.

A similar transition is undertaken by the troubled economy of Iran. Coming out from sharp protests for women’s rights, Iranian economy has taken a hit on the exchange rate front and if it weren’t for its autocratic government and its military ties, the economy would have collapsed. What do these exchange rate numbers mean? Do we have economic theories which help us understand the level of exchange rates or do they only explain changes in exchange rates?

Finally, while there are countries which must bear the burden of depreciation, there are others who either order a new currency, fix the exchange rate, or dollarize. The point of transition to other currencies is that you are taking a burden to reset your exchange rate and are committed on the forex front, which would then imply that you must take a mild slowdown on the domestic front because the appreciation makes things expensive in the domestic economy. It can also come with severe wage repression. Imagine you were paid 5000$ per month for the last 15 years but the next month you will be paid 500$. One such economy is Venezuela’s which dollarized i.e., adopted dollar as the currency for its local transaction in 2021 after a spate of hyperinflations.

What will happen to such economies is not known, but it is unreasonable to deny that their exchange rate will not have a significant role.